North Carolina’s economy is reeling under the impacts of the COVID-19 pandemic and Gov. Roy Cooper’s drastic restrictions. With businesses locked down or only allowed to open halfway at best, families are piling on loans to keep afloat while businesses that still can are taking on enormous debts to survive. This stark reality drives the John Locke Foundation’s Carolina Rebound policy solutions to help North Carolina’s people, businesses, and economy recover as quickly as possible once these are all over.

The last thing policymakers should do is make things even harder for people trying to piece their lives back together. But that would be the effect of expanding North Carolina’s prohibition against debt settlement, which is what House Bill 1067 would do. Currently, debt settlement companies in NC cannot receive their fee until after their client’s debt has been settled. The bill would not even allow debt settlement with that consumer protection.

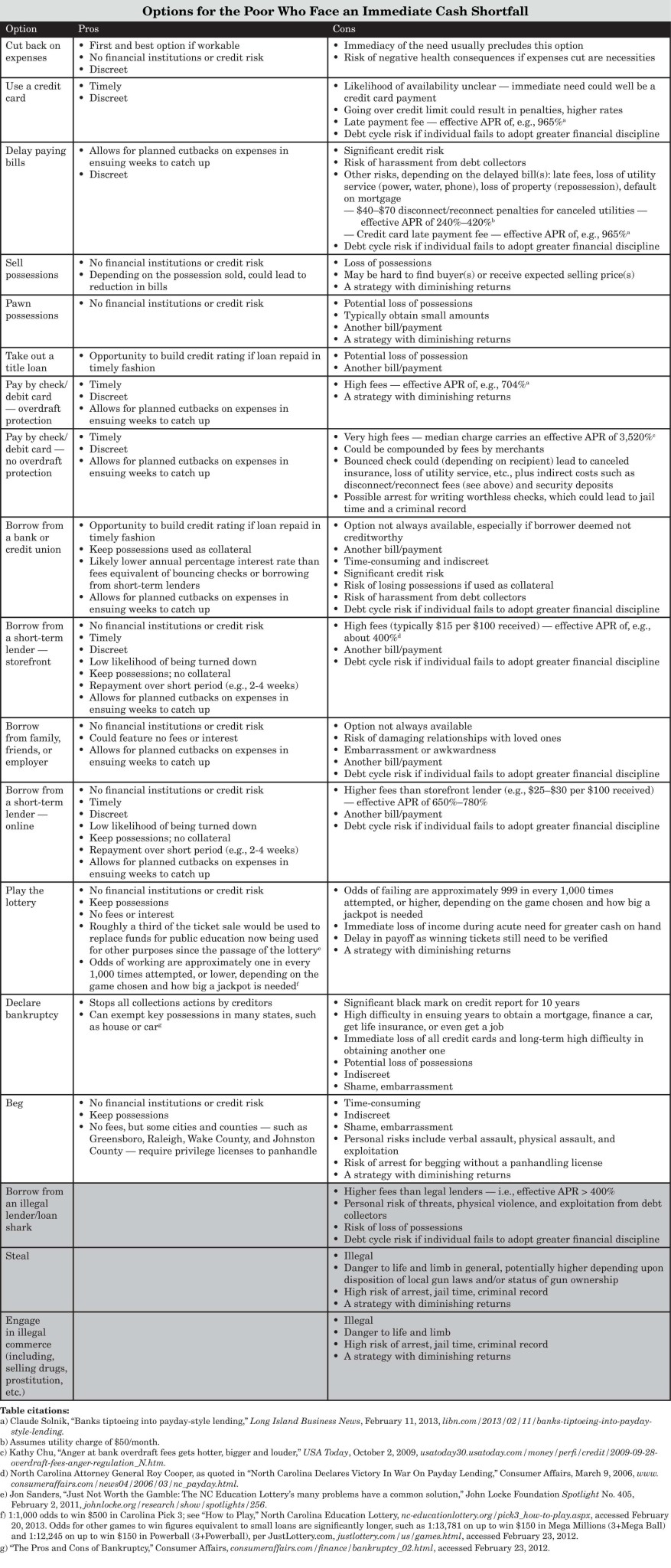

In so doing, it would remove an option from desperate debtors in NC. It would force more debtors to declare bankruptcy instead.

The ostensible reason for the bill is familiar. It seems compassionate to prevent people in a bad situation from making a choice that people in better situations would not make. But like so many other examples of government creating compassionate-seeming bans, this prohibition would have net negative outcomes for people owing to unforeseen, unintended consequences.

A North State Journal op-ed from Tomas Gordon, CEO of the debt settlement firm ClearOne Advantage, explains how debt settlement works for those who need it. A reasonable reader could infer what the loss of that option would mean for those who needed it:

Debt settlement offers financially distressed consumers a federally regulated, private-sector alternative to bankruptcy, enabling them to settle their debts for less than they owe and to remain productive, contributing members of their communities. Debt settlement companies negotiate with consumers’ creditors to settle debts for less than what the consumers owe, providing a much-needed lifeline in the midst of economic uncertainty.

A May 2020 study by Harvard Kennedy School Professor Will S. Dobbie found that “individuals enrolling in debt settlement programs receive an average debt write-down of 33.2% on settled accounts after accounting for fees.” The same study found that, on average, consumers in debt settlement programs see $2.64 in debt reduction for every $1 in fees.

In North Carolina, that translated into more than $71 million in net consumer savings in 2018 alone, savings that were used in their communities to buy groceries, pay rent and keep their families together. These are savings – and local spending – that would be lost if HB 1067 were to become law.

Banning debt settlement would also destroy a legal industry in North Carolina (and therefore more jobs). According to Gordon, debt settlement is currently a $63 million industry here. It would likely be stronger in the coming years, however, because of the crushing debt expansion owing to COVID-19 and Cooper orders.

Avoiding bankruptcy with a net reduction in debt can be a rational choice

The issue reminds me of North Carolina’s ban on short-term lending. It, too, originated with trying to protect people in desperate financial need from being taken advantage of by companies that earn money helping them out of it. But it also ignored the worse options that those consumers were forced into with that choice removed.

From a distance, paying a fee to someone to help settle your debt sounds like being taken advantage of when you already can’t afford it. Closer up, however, seeing your debt reduced by two and half dollars for every dollar you pay in fees sounds like a rational decision, especially to avoid bankruptcy and the fallout from that.

Worse outcomes tend to happen when paternalistic policymakers decide that other people are making irrational choices that aren’t in their best interests and the only way to save them is to take those choices away. A general rule of thumb for policymaking should be that more choices are better.

{kind=link}