The U.S. Census Bureau recently released its report on health insurance coverage for 2018. The total number of individuals without health insurance increased from 2017 to 2018. Many media pundits and health scholars contend that these numbers are proof that the Trump administration is attempting to “sabotage” the Affordable Care Act (ACA or Obamacare). However, this notion does not hold up to scrutiny.

In this research brief, I will examine some of the findings from the Census Bureau report and put them in the context of some of the larger forces at play in the health care market.

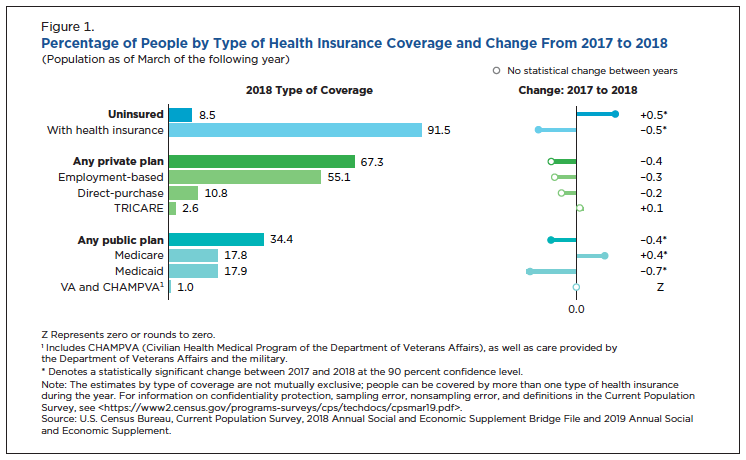

Overall Health Insurance Numbers

Figure 1 provides a breakdown of the coverage numbers from the report. The left side of the chart shows coverage by source, and the right side shows the percentage point change from the previous year. Someone would need to have coverage for at least part year to be counted as insured. If someone had no health coverage for the entire year, they were considered uninsured. In 2017, 7.9 percent of Americans or 25.6 million individuals didn’t have insurance. This number ticked up slightly to 8.5 percent or 27.5 million individuals in 2018.

Of the overall insured population in 2018, 34.4 percent of Americans had public insurance, such as Medicare or Medicaid, and 67.3 percent had private coverage. Employer-sponsored coverage covered 55.1 percent of Americans. Public coverage decreased by 0.4 percentage points overall. Medicare increased 0.4 percentage points, covering 17.8 percent of the population, while Medicaid coverage decreased by 0.7 percentage points to 17.9 percent of the population. The category for children under the age of 19 who were uninsured increased by 0.6 percentage points to 5.5 percent.

What do these numbers mean?

Critics of the Trump administration have seized on the overall insured number as proof that the current administration is undermining the Affordable Care Act. However, the policies rolled out by the administration suggest a much different stance. While the overall number of uninsured individuals did rise in 2018, we shouldn’t focus on this number as much. Across the country, Medicaid enrollment decreased by 0.7 percentage points. Given the strong economy and low unemployment, we should be encouraged to see a decrease in Medicaid rolls due to increased wages that make some ineligible for Medicaid.

Other decreases in the insured number stem directly from the Affordable Care Act’s flawed design. When purchasing a plan on the ACA’s exchanges, an individual may receive premium subsidies that correspond to your income. Some at the top of the income ladder do not receive subsidies. Those on the higher end of the income scale have continued to drop individual insurance coverage due to the cost of the plans. Former special assistant to the President at the National Economic Council, Brian Blase explains:

The number of uninsured Americans in households with income above 400 percent of the poverty line increased by 1.1 million from 2017 to 2018, and the number of uninsured in households with income above 300 percent of the poverty line — about $75,000 for a family of four — increased by 1.6 million. (Most other income groups saw small year-over-year changes in the number of uninsured.) These are people in the middle class, often without an offer of employer coverage, who are playing by the rules and simply can’t afford Obamacare plans since they don’t qualify for a subsidy — people the Trump administration’s health-care reforms are designed to help.

The same is likely happening in North Carolina. Individual enrollment in the ACA exchanges has declined substantially from 613,487 in 2016 to 501,271 in 2019.

Trump Administration Policies for the Middle Class

Recent Trump administration policies are designed to provide relief for groups that are fleeing the ACA exchanges. While repealing the Affordable Care Act and allowing each state to implement its own reforms would be the preferred course of action, the administration has been able to introduce some policies through executive order.

Those who don’t get insurance from work have minimal options. As we see with the data above, when the only option is an ACA plan without subsidies, some may be forced to go without coverage simply because they can’t afford the products offered on the exchanges. Fortunately, three policies championed by the current administration have provided more options for those who were only left with ACA plans. Association health plans; short-term, limited-duration plans; and health reimbursement accounts have all been bolstered to help individuals access more options.

The ACA did provide coverage for some who previously did not have it, but others were harmed by the ACA. Now, a few years after its implementation we see that many people can’t afford coverage due to rising premiums and no subsidies. This phenomenon is likely the reason for the decline in insurance coverage, not “sabotage” as so many have claimed.