It’s that time of year again. Time to renew your health plan, that is.

The Affordable Care Act’s 2017 health insurance enrollment period is beyond its midpoint, and consumers in North Carolina are facing an average 14 percent rate increase.

This comes as no surprise, considering that premiums have doubled within the past four years due to the federal health law’s costly consumer protections that it imposes on private insurance companies. Yet, these “consumer protections” are worthless for many middle-class Americans if it means they can’t even afford to use their health insurance.

What is surprising, however, is that for people who can afford their health insurance, they still run the risk of encountering financially ruinous medical bills.

Welcome to the world of surprise billing.

Surprise Billing – What is it?

Before diving into the issue of surprise bills, it’s important to first talk about the concept of balance billing. For certain health care services, some health plans require policyholders to pay the difference of what a provider charges an insurer and the amount the insurer pays that provider. So, to keep out-of-pocket costs as low as possible, it’s critical for policyholders to seek care by providers and health care facilities that participate in their health plan’s network. “In-network” providers agree to an insurer’s reimbursement contract.

Balance billing, however, can end up blindsiding patients when they are unexpectedly charged for out-of-network services that are 20-40 times higher than the going in-network rate. Hence the term “surprise billing.”

The conflict isn’t all that uncommon for emergency care. Even when a patient makes sure to go to an in-network emergency room, there’s no guarantee that the attending health care providers are also in-network. One in five health claims for emergency services are submitted by out-of-network providers, reports the New England Journal of Medicine. This is because many emergency physician groups aren’t employed by hospitals. As independent contractors who work at multiple facilities, they negotiate insurance payment separately.

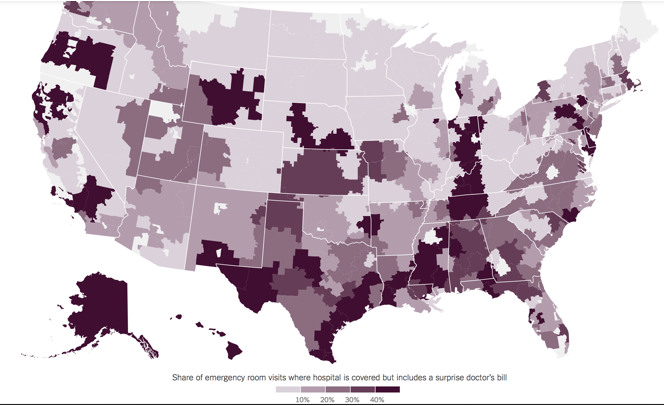

The map below lays out where patients across the country are more likely to receive a surprise bill for emergency care when presenting themselves at an in-network facility. In North Carolina, these encounters are much more prevalent throughout the southeastern region of the state. In Columbus County, for example, out-of-network emergency physician groups have reportedly charged rates as high as 1015% of what Medicare pays.

Source: New York Times

The ER isn’t the only point of entry in the health care system where patients can be exposed to surprise bills. It can also happen after elective surgery. Let’s say that a patient schedules a knee replacement procedure. The patient is informed that the surgeon and the hospital are in-network but has no idea that the anesthesiologist isn’t. A few weeks later, the patient is hit with a medical bill for anesthesia at a surprisingly high out-of-network rate. Similar to emergency physicians, anesthesiologists may also be out-of-network if they aren’t salaried by any hospital.

Factors Contributing to Surprise Billing

Surprise billing will likely become more widespread as result of the ACA’s so-called consumer protections. Under the ACA, insurers are required to cover more benefits, can’t deny coverage for a policyholder’s pre-existing condition, and are prohibited from accurately pricing people’s risk based on their health status. They also can’t charge older policyholders’ premiums more than three times the amount of a young person’s premium.

All these protections come with a hefty price tag, which explains why policyholders are experiencing multiple rounds of double-digit premium increases over the past four years.

What’s an insurance company to do?

The Rise of Narrow Networks

Many are responding by designing narrow networks to control costs. The ACA may have taken away most strategies insurers typically use to keep premiums and out-of-pocket expenses in check, but insurers still have the freedom to build plans that feature fewer provider choices.

Almost half of ACA plans feature both small and extra small hospital networks. Small networks cover less than 70 percent of local hospitals, while extra small networks give policyholders access to fewer than 30 percent of local hospitals.

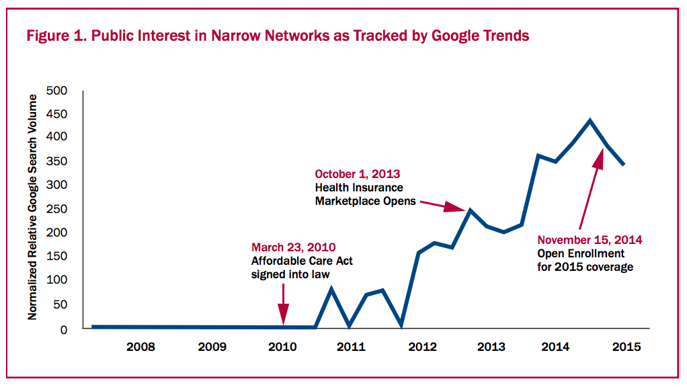

For some, narrow networks aren’t necessarily a bad thing. Price-sensitive consumers are willing to sacrifice fewer health care options in exchange for lower premiums and cost-sharing. These plans are also popular for people who don’t use the health care system often. The chart below shows that, even before the ACA exchanges were first implemented in 2014, an increasing number of people expressed interest in narrow network options.

Source: Leonard Davis Institute of Health Economics, Robert Wood Johnson Foundation

But a higher prevalence of narrow networks could very well trigger more surprise bills.

So, how is this problem being addressed?

Many states have passed laws that remove the patient from a surprise bill situation and leave the payment dispute to be sorted out between the out-of-network provider and the insurer. Other states require that patients only pay for in-network cost-sharing if they are unexpectedly billed by an outside network provider, while the insurer pays the difference. Some laws also place limits on how much insurers pay outside providers.

These policies certainly have good intentions, but removing patients from billing discrepancies is a barrier to gaining more consumer control in the health care space. The issue with surprise billing points to the health care industry’s biggest problem – lack of price transparency.

In places where price transparency does exist, there are no surprise bills. That’s because patients know how much their surgery will cost before they go under the knife.

This is exactly how the Surgery Center of Oklahoma (SCO) operates. SCO has completely opted out of insurance contracts and offers cash pricing for various elective procedures. Just as it’s proven to save uninsured and insured patients, it’s also extremely valuable for employers who are at-risk for most of their employee’s health care claims. Because SCO prices are lower than their competitors, it’s not unusual for out-of-state employers to pay for their employee’s travel expenses in addition to the cost of their outpatient procedure.

Imagine if more health care settings worked directly for patients, not insurance companies. Patients would have more leverage over the quality of health care and its cost because the people who are delivering health care would only thrive based on patient satisfaction. Such a drastic transition would, in fact, make for a true marketplace in health care, and surprise billing wouldn’t be the problem that it’s become today.