The Wall Street Journal reminds us that five years ago today, President Obama signed the massive stimulus bill into law.

He did this because, apparently, White House message crafters were still five years out from discovering what a great thing it is for people to be “liberated” from the “chains” of employment. The president is, of course, allowed to “evolve” a position as the politics of the day require. Media will treat any new evolution like tube socks at Christmas from Granny: smiles, effusive praise, later to tuck them away and forget about them.

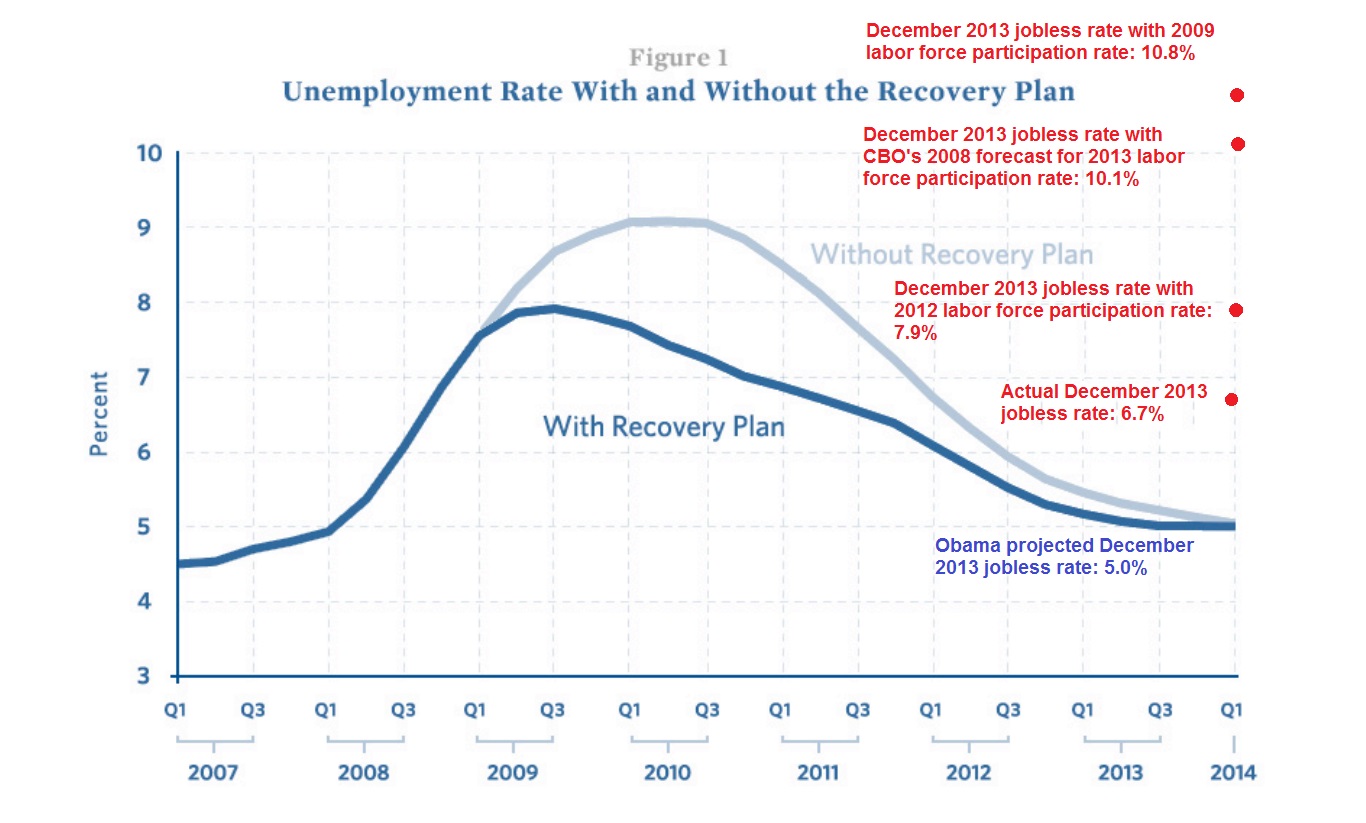

Back then, the incoming Obama administration put out a report explaining that this spending was extremely necessary — to keep unemployment from exceeding 8 percent, instead of peaking at 9 percent. (With the stimulus, it “unexpectedly” exceeded 10 percent within the first year.)

The Obama administration also projected that, whether the stimulus was passed or not, by 2014 (which is, you know, now) unemployment would have fallen to 5 percent (the long-run “natural rate” of unemployment). If you think the Obama administration believes unemployment will never return back down to 5 percent, however, you’re wrong; they predict it will happen sometime after 2023.

As the WSJ writes,

The $830 billion spending blowout was sold by the White House as a way to keep unemployment from rising above 8%. But the stimulus would fail on its own terms. 2009 marked the first of four straight years when unemployment averaged more than 8%. And of course the unemployment rate would have been even worse in those years and still today if so many people had not quit the labor force, driving labor-participation rates to 1970s levels.

The Obama White House had been egged on by liberal economists like Paul Krugman, who in November of 2008 recommended a stimulus of at least $600 billion. Team Obama worked with Democrats in Congress to exceed his minimum request by more than 30%. But after the failure of the stimulus the same liberal economists who had enthusiastically supported the plan would claim that its main flaw was that it was too small.

This ongoing failure is so roundly ignored by the president’s media yes-men (i.e., “President Obama said reporters praise his economic proposals as ‘great’ and tell him they are ‘all good ideas'”) that they are reliably caught off-guard by “unexpected” disappointing economic data, month after month.

Via James Pethokoukis, here is the disposition of the graph as of December 2013 (click the image for a larger version):

WSJ concludes:

The failure of the stimulus was a failure of the neo-Keynesian belief that economies can be jolted into action by a wave of government spending. In fact, people are smart enough to realize that every dollar poured into the economy via government spending must eventually be taken out of the productive economy in the form of taxes. The way to jolt an economy to life and to sustain long-term growth is to create more incentives for people to work, save and invest. Let’s hope Washington’s next stimulus plan is aimed at reducing the tax and regulatory burden on American job creators.

This year North Carolina’s leaders changed course on economic policy, reducing tax burdens and regulatory burdens and bringing unemployment insurance benefits more in line with other states’, a move that dropped the state from the federal government’s extended UI benefits program. Early returns on those changes, even as the state’s economy pulls against its federal drags, have been encouraging.