I just came across this summary/comparison of the House and Senate’s tax reform proposals published by Forbes. It is really quite good at laying out the details in a side by side approach, covering every aspect of the two pieces of legislation.

To be quite frank, after seeing the details of these proposals they are nowhere near as good as I had initially thought. Here is one, of many, examples. In the House bill, for couples earning $1 million a year or more, the effective marginal tax rate will actually be 45.6 percent, a rate that President Obama couldn’t have dreamed of getting Congress to approve.

The reason for this is that, for those earning over $500,000 a year, the statutory rate will remain at 39.6 percent. But once a couple’s income reaches $1.2 million ($1 million for single filers) there is a clawback provision of the bottom 12 percent rate. This means these taxpayers lose any benefits from the 12 percent rate, which for a married couple would apply to the first $90,000. The lowest rate for couples earning over $1 million won’t be 12 percent; it will be 25 percent. At the $1 million income level, this would add almost $25,000 to a married couple’s tax bill. And it would go up from there. Here’s how Forbes describes it:

HR 1 proposed four brackets: 12%, 25%, 35% and 39.6%. Taxpayers earning more than $1 million (if single, $1.2 million if married) would also be required to “clawback” the benefit of the 12% bracket at a 39.6% rate, increasing their tax by the excess of the 39.6% rate over the 12% rate on the first $45,000 of income (if single) or $90,000 (if married). This amounts to an increase in tax of $12,420 for single taxpayers and $24,840 for married, and an effective top marginal rate of 45.6%.

Punitive? I would say so.

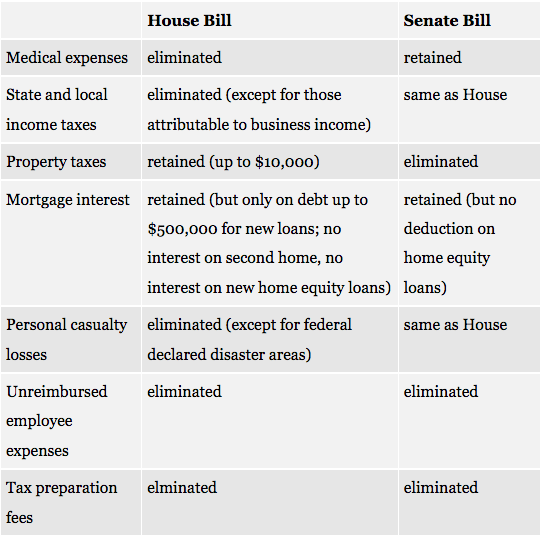

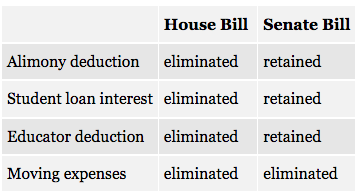

There are other changes that are being proposed which simply reflect a blind allegiance to base broadening, and probably revenue raising, without regard to the economics of taxation. In addition to the elimination or partial elimination of deductions for state and local taxes, which has been covered extensively, another deduction that makes sense, but is eliminated in both bills, is the deductibility for moving expenses. (See tables below.)

Itemized Deductions

Source: Forbes

Other Popular Deductions

Source: Forbes

But sound economics suggests that if a move is a work-related expense, it should be deductible. This is because, whether we are talking about businesses or individuals, any costs associated with generating income should be deductible. It doesn’t matter whether it’s a construction company buying a bulldozer or an individual moving across the country. For the same reason, student loan interest should be deductible and so should unreimbursed employee expenses. But these valid deductions could easily become a thing of the past.

The fact is that there should be a symmetry between businesses investing in physical capital and individuals investing in human capital. All such expenses should be deductible from income before it becomes part of one’s tax liability. The House and Senate are clearly moving in that direction when it comes to business taxes, but this basic principle, in large part, goes unrecognized for individuals earning their living as employees.

Forbes has produced a very useful document for people trying to figure out what’s what in these tax bills. The link to their article is worth keeping handy as Congress works toward passage of comprehensive tax reform.