The dominant organization with regard to state accounting standards, The Governmental Accounting Standards Board, has recently refined its guidelines for reporting on pensions.

I can see people’s eyes glazing over already, but stay with me. This organization, which to a large degree has facilitated misleading, cash-basis accounting practices, is publicly recognizing the problem of miscalculated pension liabilities and recommending a "more faithful representation of the full impact of these obligations."

As I note in one of my Agenda 2012 articles, the prevailing approach of North Carolina’s controller is to discount future obligations at 7.25 percent per annum. This rate underestimates the present value of these liabilities given the near certain obligation to pay. A lower rate of 4 percent or less would be more accurate, and even the Congressional Budget Office has recommended such an adjustment.

Consider the example of a $50,000 pension payment, to go out in 20 years time. A discount rate of 7.25 percent equates to a value of $12,300 right now. On the other hand, a discount rate of 4 percent equates to a present value of $22,800, almost twice the liability.

GASB has not had the courage to require all pension plans to come down to a reasonable discount rate, in line with normal municipal borrowing rates (consistent with the cost of paying other entities to take over the debts). However, for all underfunded pensions (pp. 3-4), such as the majority in North Carolina, they do recommend this change.

The distinction is confusing, since it imposes the burden on pension plans least able to comply. So whether state controllers will carry out this revision — they are not legally obliged to do so — remains to be seen. It goes into effect in 2014.

Either way, recognition from this organization carries at least symbolic value. States have been underreporting and concealing their obligations, and GASB no longer wants to be party to it.

Ideally, state officials would also measure pension liabilities as an ongoing expense, since accuracy is not the only problem. That is why I encourage legislators to implement FACT based accounting, as promoted by the Institute for Truth in Accounting.

Image of the week!

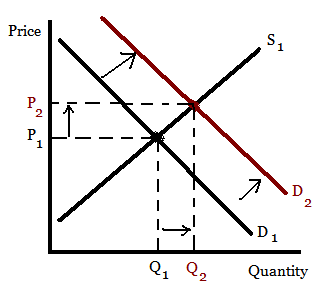

Many of you will have seen this one before, probably when studying for an introductory economics course. However, when confronted in an interview alongside Peter Schiff of Euro Pacific Capital, an economist with the Progressive Policy Institute repeatedly denied such a relationship with college tuition.

The logic is painfully simple. Greater loan availability, due to federal sponsorship, increases the quantity demanded at each price (tuition) level. That leads to higher prices and increased quantities traded. Tuition growth at 5 percent beyond inflation over the last five years and record student participation this past academic year stand as compelling evidence.

Here is that interview, in which Peter Schiff does an excellent job countering Diana Carew.

Notes

- As some of you may already know, I am highly active on Twitter and glad to engage with more people through that medium. If you would like to follow me, my username is@FergHodgson (si prefiere espanol @Fergusito).

- One of my favorite sites for North Carolina and national pro-liberty news and commentary is FoundersTruth.org. One could accurately describe them as paleoconservative, with great respect for constitutional, limited government. Recently, the organizers started a new Facebook page for likeminded people, and I encourage people to consider following it here.

- John Hood, president of the John Locke Foundation, interviewed me on Friday, as he sat in for Bill Lumaye of WPTF 850. If you would like to listen in, here is the MP3 from the 3 to 4pm hour.

Click here for the Fiscal Insights archive.