- The North Carolina General Assembly is still finalizing a two-year budget

- Budget proposals from the House, Senate, and governor would have varying effects on North Carolina’s fiscal future

- Spending restraint, tax cuts, and considerable savings would contribute to more opportunities and bigger paychecks for North Carolina families

Negotiations are underway in the North Carolina General Assembly as representatives from the House and Senate debate the conference budget. Two months of this fiscal year have already passed. As North Carolinians anticipate the possibility of having a traditional state budget, the House, Senate, and Governor’s office have offered contrasting proposals that would have substantial effects this fiscal year and beyond.

Legislators have a broad spectrum of options to choose from with regard to spending, savings, and teacher pay, among others. This budget also has the potential to give significant funds back to taxpayers and spur state growth.

The budget proposals have many additional, important elements regarding health care, capital spending, emergency powers, and more. This analysis, however, focuses on top-line numbers in a handful of key areas.

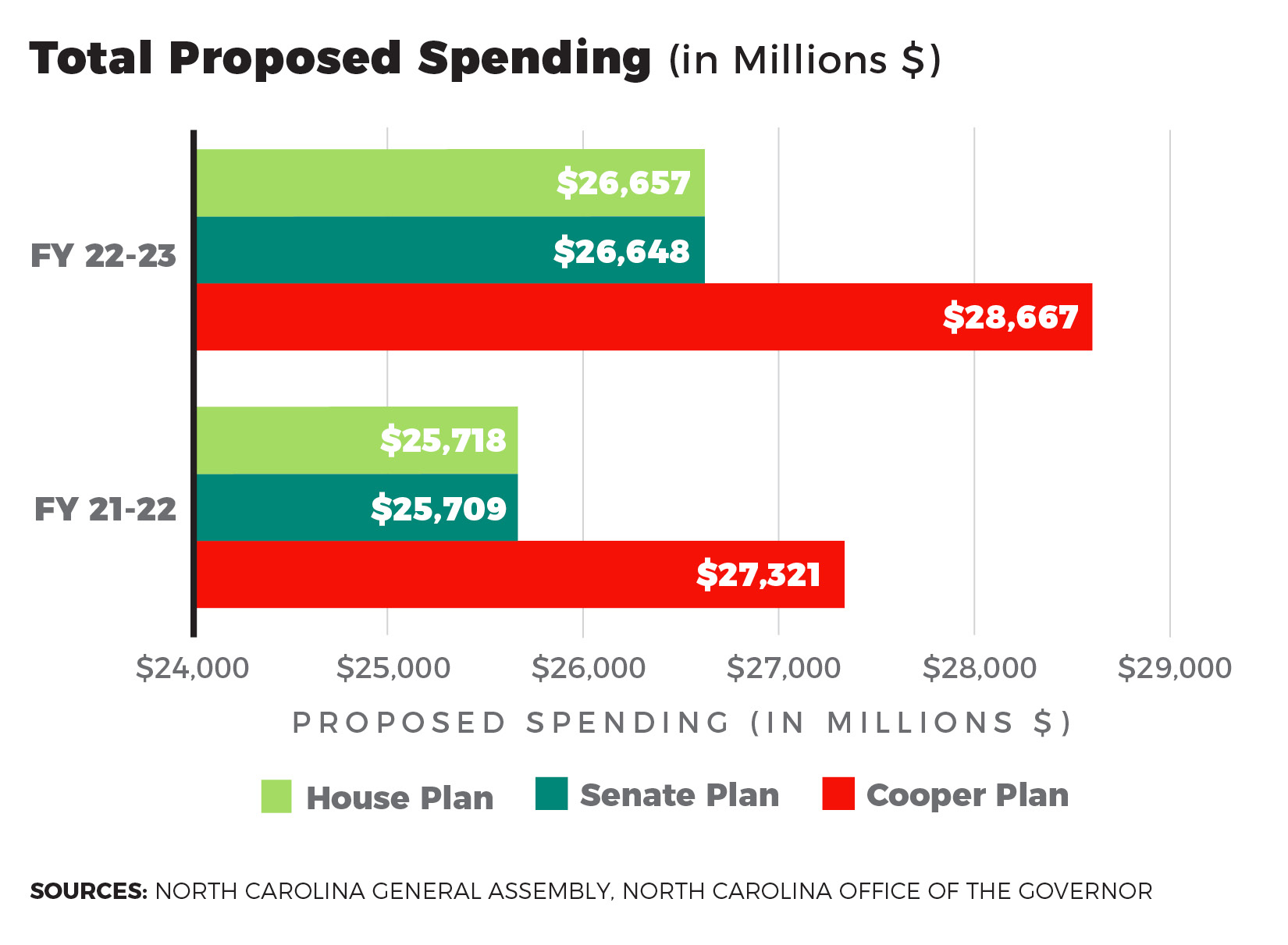

The Price Tag

As shown below, the budget recommended by Gov. Roy Cooper in March 2021 would spend noticeably more than the House and Senate plans. At $27.3 billion, the governor’s recommendation would be a year-over-year spending increase of 14%, or $3.4 billion. Earlier this summer the Republican-led legislature judiciously agreed to a $25.7 billion spending limit for the first year of the biennium.

Overspending produces unsustainable budgets, which legislators have historically paid for with tax hikes and state employee layoffs. During the last decade, however, conservative leadership has fostered a business-friendly, fiscally responsible environment in North Carolina. This restraint allowed the state to weather the economic slowdown from Cooper’s pandemic lockdowns. More government spending imposes a greater burden on the economy by diverting more scarce resources from the productive sector to the hands of politicians. As Milton Friedman stated, government spending is the true tax.

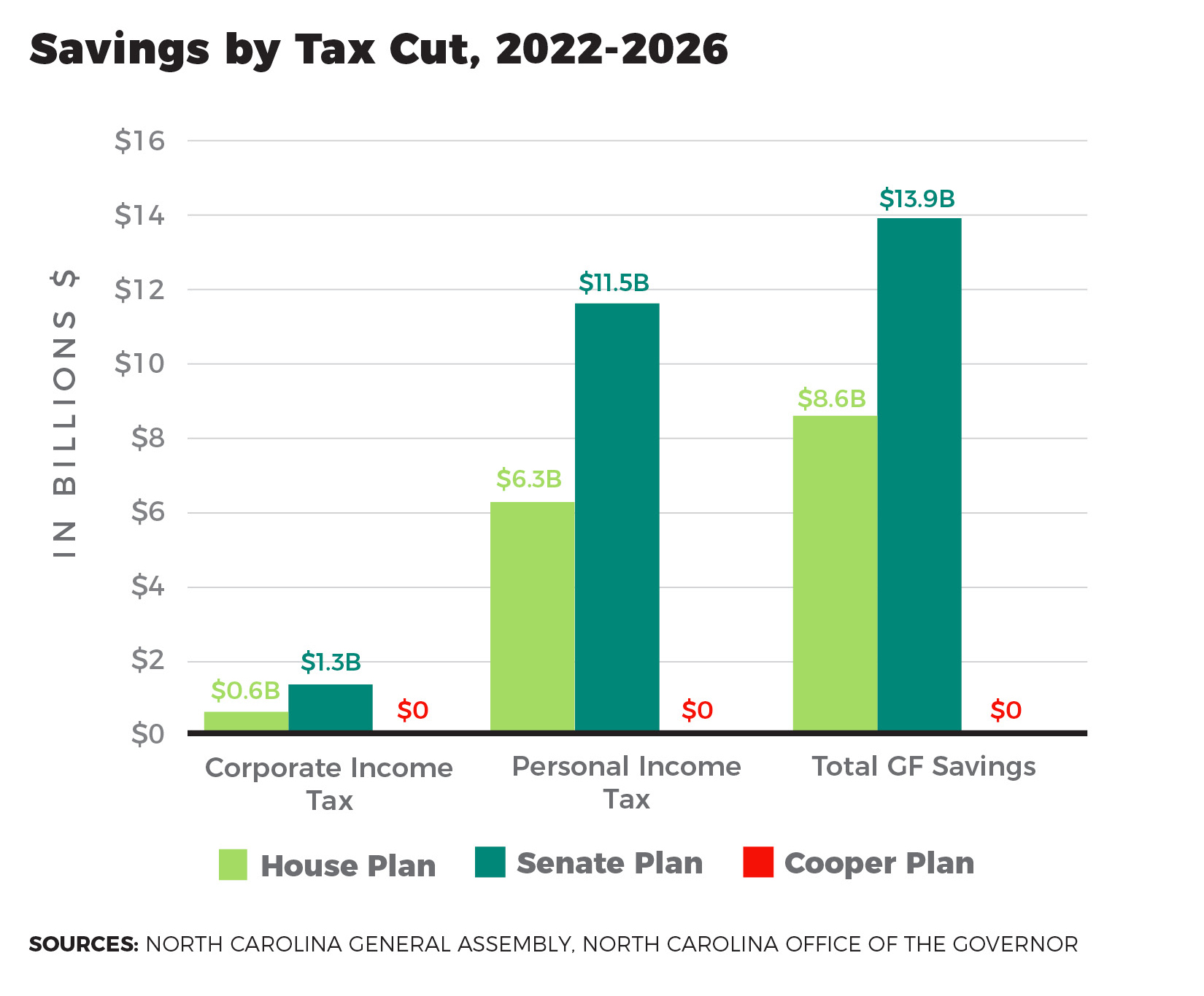

Taxpayer Savings

Both the House and Senate included personal and corporate income tax cuts in their proposals. Those could mean huge savings to North Carolinians. Cooper’s recommendations did not include tax cuts.

The graph below shows the aggregate savings for fiscal years 2022–2026 (some of the proposed cuts would occur in 2026) to taxpayers in the House and Senate plans’ personal and corporate income tax cuts. It also shows the total General Fund impact of those proposed changes. The personal income tax totals include the savings from the standard deduction increase as well as other changes (the increased child deduction for the Senate plan, for example). Total General Fund impact includes changes to miscellaneous taxes such as modified cigar taxes, property tax changes, and pandemic-related provisions such as Paycheck Protection Program (PPP) loan reductions. The Senate’s plan would give the most money back to working North Carolinians.

Although the corporate income tax rate reduction results in a smaller dollar amount of savings, research has shown that the state corporate income tax is the most harmful state tax to economic growth. The corporate tax is a tax on workers and reduces wages and employment. Cutting or eliminating corporate income taxes would mean more jobs and bigger paychecks for North Carolina families.

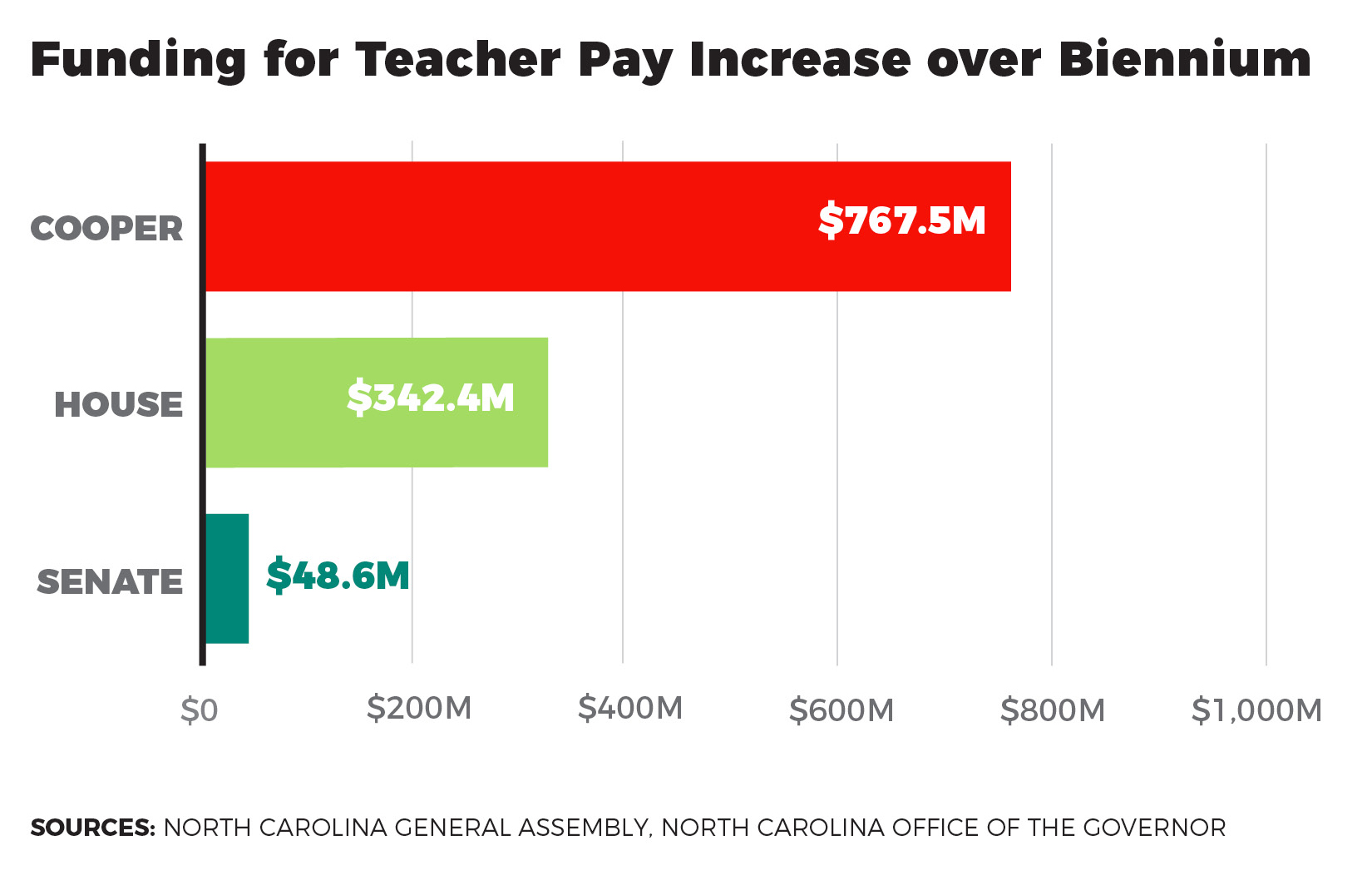

Teacher Pay

Each budget proposal would increase teacher pay, although the approaches differed. Gov. Cooper included a 10% average increase in teacher pay over the biennium. The Senate included a 3% average increase, and the House called for a 5.5% increase in pay over the same period. The table below shows the estimated dollar amounts associated with just the proposed teacher salary increases over the biennium. Additional increases to teacher compensation proposed in those budgets, including bonuses, are described below but are not reflected in the chart.

Cooper’s plan would restore master’s pay for teachers, despite evidence showing master’s degrees for teachers do not translate into better student achievement. His plan would also give a one-time bonus of $2,000 to teachers (and all public school personnel) as well as additional $1,000 bonuses to all education employees for each year of the biennium.

In the House proposal, the pay increases would not be evenly distributed and would favor veteran teachers. The House plan would also reinstate an increase in pay of 10% to teachers with a master’s degree (an estimated $8 million annually). Additional bonuses would be awarded to certain math and reading teachers based on student performance and to teachers working with students with visual and hearing impairments.

The Senate plan would give additional $300 bonuses across the board to teachers. The Senate plan would increase each step of the teacher pay schedule by 0.25%. Those increases combined with others would result in a 3% average increase in pay for the biennium.

Separate from the teacher pay issue, the plans would approach school choice differently. For example, Cooper’s plan would eliminate the Opportunity Scholarship Program, which allows working parents access to funds to send their children to the private school of their choice, while the House and Senate plans would expand eligibility for the program.

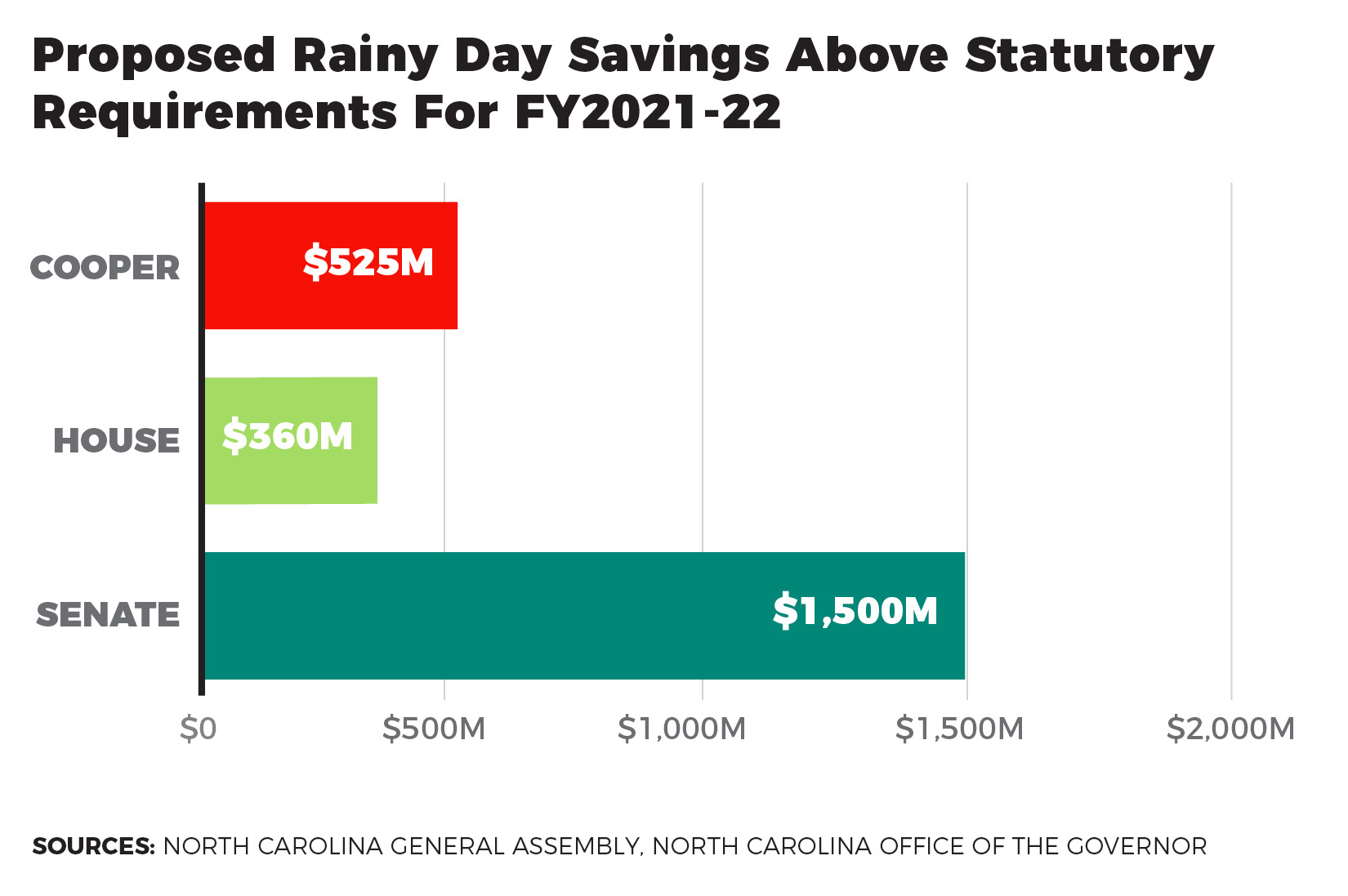

Rainy Day Fund

State law requires 15% of the estimated growth in state tax revenues to be allocated for the Rainy Day Fund (the Savings Reserve) for each fiscal year of the upcoming biennium. The graph below looks at the proposed contribution to the Savings Reserve on top of the statutory requirement for the first fiscal year of the biennium only. Savings Reserve funds can be allocated only by the General Assembly.

Given that the three budget proposals were released at different times, the base Savings Reserve requirement differed for each proposal. When the governor released his budget recommendations, there was a much smaller amount of anticipated revenue. The House and Senate had knowledge of the larger expected revenue. Even so, the House was much stingier with the savings than the Senate.

Conclusion

North Carolina workers continue to anticipate the benefits that may materialize with a budget. Although state law ensures that the government does not shut down without a budget, savings and other projects are postponed with the stalled process.

Legislative leaders’ decision to set spending limits is great news for taxpayers. State government should not be allowed to grow unfettered at rates faster than the state economy that pays for it. Along with this restrained spending, legislators should prioritize tax reforms that incentivize economic growth by eliminating the corporate income tax, for example.

The conferees are expected to come to an agreement on the bill before presenting the plan to Gov. Cooper, who has never signed a traditional state budget bill into law. However, with several Democrats on board with the House and Senate versions of the bill, there is no guarantee a potential veto from the Governor would stand.